I. Introduction

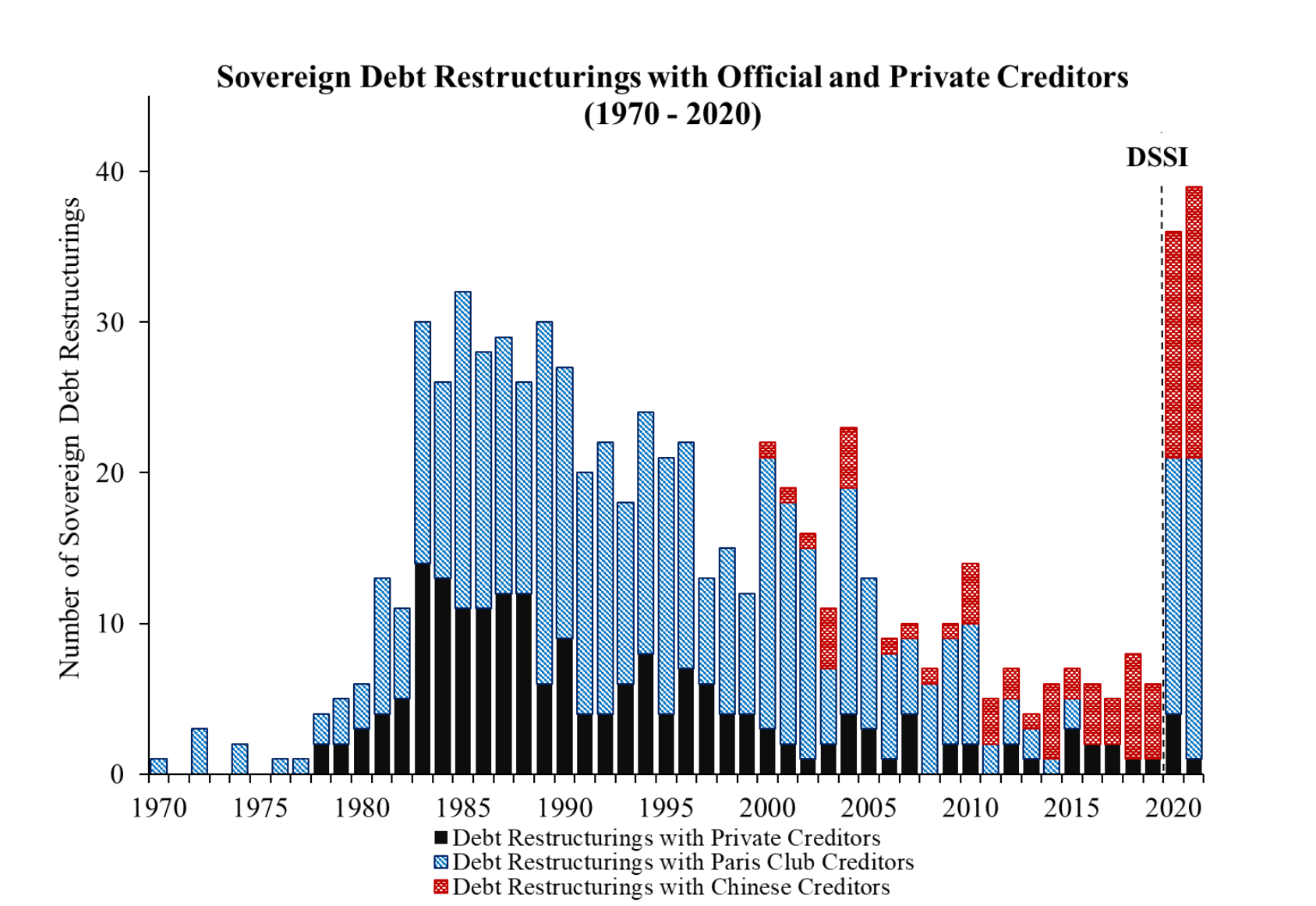

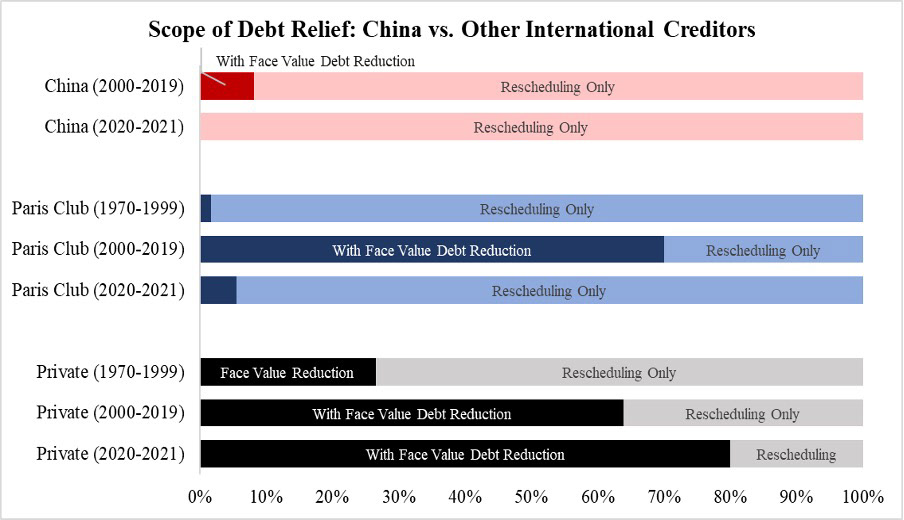

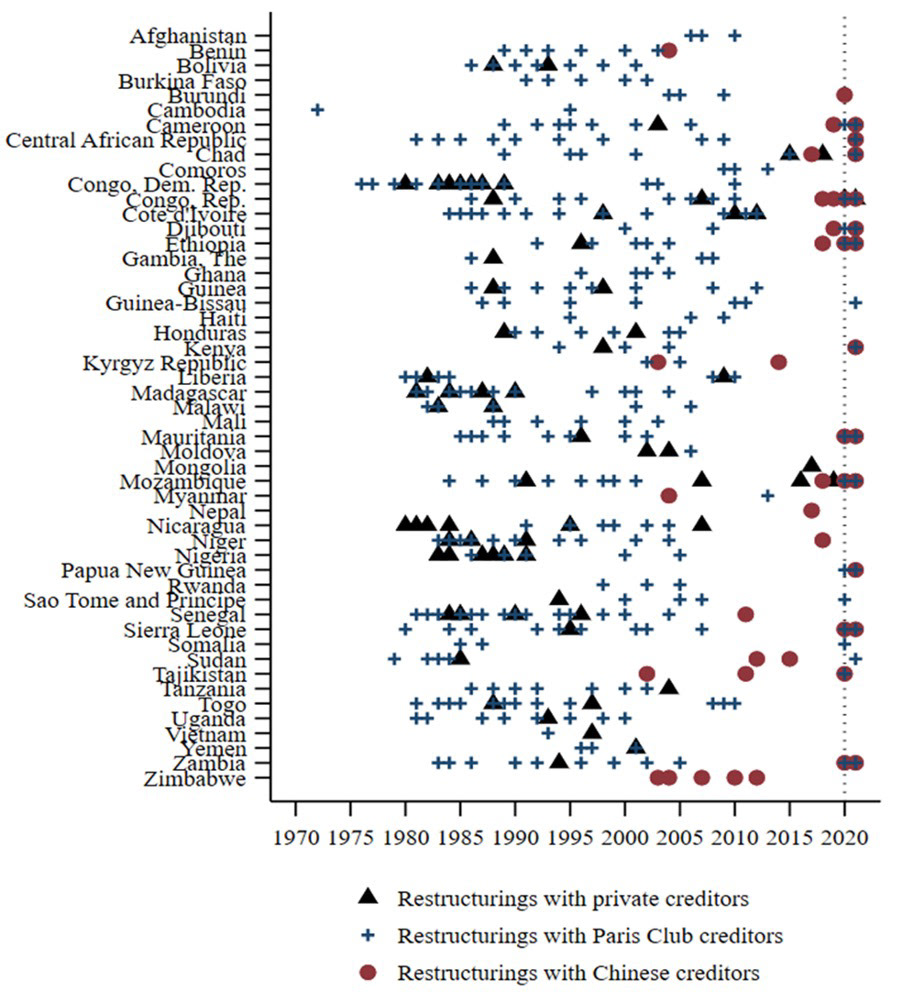

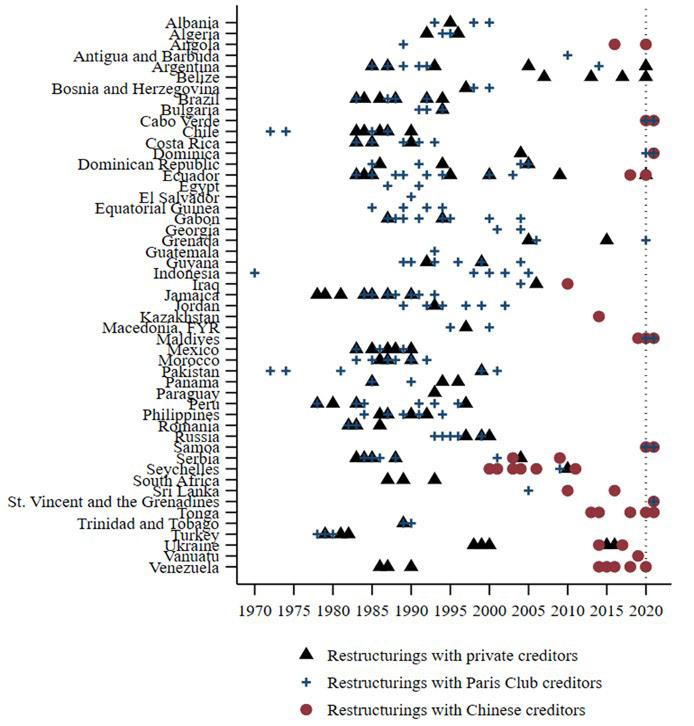

Since 2000, China has become the largest bilateral creditor to emerging markets and developing economies, providing record levels of capital through the Belt and Road Initiative (BRI). However, following a decade-long boom of overseas lending, China’s BRI has come under pressure as many debtor sovereigns experience financial distress, facing debt servicing difficulties or are in outright default as shown in Figure 1. Chinese state-owned banks have responded to this challenge by prioritizing debt rescheduling with no face-value reductions. (reference 1) Historically, these “no-haircut” debt restructurings mirror the strategy employed by official creditors of the Paris Club and private external creditors from 1970 to 1999, which led to back-to-back maturity extensions or “serial restructurings” of the same debt that mitigated short-term losses for creditors but prolonged debt cycles for borrowers. (reference 2)

Figure 1: Sovereign Debt Restructurings with China, Paris Club, and Private Creditors

The economics literature has long explored the costs of sovereign restructurings and defaults, although it has primarily focused on the relationship between private external creditors and debtor sovereigns. On the creditor side, it is well-documented that serial restructurings often result in deeper creditor haircuts by the time the debt is resolved. Additionally, lenders to lower-income and first-time issuers often experience significantly higher losses, with geopolitical shocks, such as wars or revolutions, driving the deepest haircuts. (reference 3) On the debtor side, empirical literature has converged on the central finding that restructurings and defaults are followed by output losses. While there is little doubt that real GDP provides an essential measure of economic costs, there remain questions on how those costs translate to other measures of health.

This paper seeks to contribute to the literature in two ways by tackling the question: What are the long-term consequences of China’s debt restructuring practices from 2000 to 2020 on the health and welfare of populations in debtor countries? First, this study narrows its focus to China between 2000 and 2020, addressing the absence of research on the social implications of its lending practices on debtor populations. Second, it bridges a significant gap in the literature by examining the relationship between sovereign serial restructurings and health or other welfare-related indicators, an area that remains virtually unexplored.

Our analysis examines the social and economic effects of serial debt restructurings across 77 episodes from 1970 to 2020. The key indicators analyzed include child mortality rates, life expectancy, anemia prevalence, and government health spending, alongside economic measures such as GDP per capita and debt service obligations. The findings reveal that serial restructurings lead to substantial and long-lasting social costs. Each restructuring is associated with a 3.7% increase in child mortality rates, translating to approximately 2 additional child deaths per 1,000 live births in a country with a baseline mortality rate of 50. Similarly, life expectancy decreases by 1.4 years per restructuring, with lingering effects reducing life expectancy by an additional 1.08 years in the subsequent year. Anemia prevalence among children under five rises sharply, increasing by 57.3 to 70.3 percentage points per restructuring, though this may reflect deeper systemic vulnerabilities in healthcare systems. On fiscal outcomes, restructurings significantly constrain public health investment, with government health spending declining by 8.2% to 10.4% per restructuring. These reductions highlight how fiscal pressures force governments to prioritize debt obligations over critical social services, exacerbating health vulnerabilities.

The trajectory of these health and economic indicators underscores the pervasive and enduring social costs of serial restructurings. Countries undergoing repeated restructurings face compounded challenges, with fiscal constraints amplifying adverse outcomes for child health, life expectancy, and public health systems. These findings emphasize the need for targeted policies to mitigate the long-term developmental impacts of repeated debt crises.

II. Literature Review

This paper builds on foundational work by Horn, Reinhart, and Trebesch (2020), whose database of over 5,000 loans and grants to 152 countries between 1949 and 2017 highlights China’s emergence as the largest bilateral creditor to emerging markets and developing economies. Their findings underscore China's reliance on two distinct strategies for addressing debtor distress: low-income countries often receive debt maturity extensions without face-value reductions, while emerging markets are typically offered rescue loans. These maturity extensions contribute to serial restructurings, perpetuating debt cycles rather than resolving them. Das, Papaioannou, and Trebesch (2012) provide a comprehensive review of sovereign debt restructurings between 1950 and 2010, highlighting that repeated restructurings are often a symptom of unresolved debt crises. They find that while interim restructurings may alleviate immediate liquidity pressures, they rarely address the underlying solvency issues, leading to prolonged economic stagnation. Graf von Luckner et al. (2024) examine serial restructurings across 205 default spells over 200 years and find that prolonged debt crises result in larger cumulative creditor losses, measured through the "Bulow-Rogoff haircut." They also emphasize that interim restructurings rarely provide meaningful debt relief and that lenders to poorer nations, first-time borrowers, and those most reliant on external creditors experience the highest haircuts. Wars or revolutions are also linked to the most severe losses. These findings directly inform the focus of this paper on serial restructurings' broader social impacts.

The effect of sovereign debt restructurings and defaults on government health spending, infant mortality rate, and other welfare indicators remain unexplored. However, the macroeconomic consequences of sovereign defaults are well-documented. For instance, Asonuma et al. (2019) find that restructurings are associated with sharp declines in GDP, investment, bank credit, and capital flows. Similarly, Reinhart and Rogoff (2009) document that real GDP per capita contracts one year before default, reaching a trough in the default year, with recovery remaining incomplete even three years later. Beyond the literature on sovereign restructurings and defaults, related studies emphasize the regressive effects of inflation crises, which often occur alongside these distressed scenarios. Easterly and Fischer (2004) describe inflation as a "cruel tax" that disproportionately burdens the poor. Similarly, Diaz Alejandro (1963) argues that currency crises in emerging and developing economies exacerbate inequality by shifting income from workers, who have a higher propensity to consume, to exporters, who tend to save more. Reinhart and Rogoff (2009) highlight that sovereign defaults are frequently accompanied by inflation surges and currency devaluations, which compound economic hardships. Additionally, fiscal consolidation measures aimed at restoring debt sustainability often lead to cuts in social programs, further intensifying the negative welfare impacts.

While these studies establish the economic and social repercussions of defaults and inflation crises, they leave critical questions unanswered regarding their broader societal costs. This paper aims to fill this gap by examining how China’s serial restructuring practices impact health and welfare indicators of debtor populations, such as infant mortality rate, the prevalence of anemia among children, government health spending, and infant life expectancy.

III. Data

Our data on Chinese debt restructurings is aggregated from three primary sources, each offering comprehensive and complementary perspectives on sovereign debt negotiations and outcomes involving Chinese creditors. The first source is Horn, Reinhart, and Trebesch's dataset on sovereign debt restructurings from 1970 to 2020, which provides a detailed account of 1,000 sovereign debt restructurings, including those led by Chinese creditors, as well as restructurings involving banks, bonds, and the Paris Club. The second source is the March 2021 update of the China Debt Stock dataset from 2000 to 2017, which focuses on direct loans issued by Chinese creditors and offers country-specific and annual debt stock estimates, facilitating granular analysis of bilateral debt patterns. The third source is the September 2020 update of the Sovereign Default and Restructuring dataset, compiled by Asonuma and Trebesch, which tracks the start and end dates of 197 sovereign default episodes and restructuring spells with foreign banks and bondholders from 1970 to 2020.

To ensure methodological consistency and avoid confounding effects, we applied several restrictions to the data. First, we excluded all instances where a country was engaged in war during the restructuring period. Second, we focused on cases where countries underwent serial restructurings without being rescued by China’s Ministry of Commerce through the provision of rescue loans. Although China has extended loans to countries prior to 2000, the dataset is further restricted to the period from 2000 to 2020, reflecting more consistent data availability and alignment with modern restructuring practices. After these exclusions, the sample comprises 36 countries that experienced 77 serial restructurings with China within a 10-year range since their first serial restructuring. For comparative analysis, we included a control group of countries to which China has lent but that did not experience serial restructurings. Instances where Paris Club and private external creditors have engaged in serial restructurings were excluded to prevent any overlap or contamination of the treatment and control groups. Additionally, we omitted data from 2021 to 2022 due to the Paris Club’s maturity extensions during this period, which were a direct result of the Debt Service Suspension Initiative (DSSI). These extensions differ from traditional serial restructuring mechanisms and are thus excluded to ensure that datapoints are comparable.

Macroeconomic variables sourced from the World Bank serve as control variables, capturing growth trajectories, external debt levels, and financial stability in countries undergoing Chinese debt restructurings. Key indicators include GDP growth rates, GDP per capita in USD, total debt service as a percentage of gross national income, external debt stocks, unemployment rates, official exchange rates, and inflation rate. Investment data, such as net inflows of foreign direct investment, provide insights into capital flows and external confidence during debt crises.

At the core of this analysis are social metrics, including infant mortality rates and life expectancy, which serve as the primary dependent variables. These metrics assess the societal consequences of debt restructurings, capturing their impact on human capital, public health, and demographic trends. FAOSTAT data, including variability in food supply per capita and prevalence of undernourishment, complement these measures by reflecting food system resilience and broader social costs of economic distress. As a note, variables requiring transformation for normality or comparability are logged to ensure robustness.

IV. Methodology

This study employs fixed-effects panel regression models to examine the relationships between serial debt restructurings and a range of social and fiscal outcomes, including infant mortality rates, anemia prevalence, government health spending, and life expectancy. Fixed-effects models are chosen because they control for unobserved, time-invariant characteristics within countries, such as baseline institutional quality, health infrastructure, or geographic factors, that might confound the relationships of interest. These models also include year fixed effects to account for global trends or shocks, such as pandemics or international economic crises, that could affect all countries simultaneously. Robust standard errors clustered at the country level address potential heteroskedasticity and serial correlation, ensuring reliable estimates. Across all analyses, independent variables include macroeconomic controls such as GDP per capita, inflation, and external debt metrics, which help isolate the effects of restructurings on the dependent variables.

A. Infant Mortality Rate

The relationship between serial debt restructurings and infant mortality rates is analyzed with log-transformed mortality rates as the dependent variable, ensuring normalized distribution and mitigating the influence of outliers. Serial restructuring is the primary independent variable, with cumulative effects accounted for by constructing a rolling 10-year sum of restructuring events since the first event. The initial model establishes the baseline relationship, while subsequent models introduce macroeconomic controls such as foreign direct investment inflows, GDP per capita, inflation, and exchange rates to account for broader economic conditions influencing infant mortality.

B. Prevalence of Anemia

The prevalence of anemia among children under one year of age serves as another dependent variable, capturing the nutritional and health implications of serial restructurings. The baseline model evaluates the direct relationship between serial restructurings and anemia prevalence, with controls for food supply per capita and inflation. Subsequent models incorporate government health expenditure to account for the role of public investment in health services, and total debt service to investigate whether fiscal constraints mediate the relationship between restructurings and anemia prevalence. These models provide insights into how restructuring episodes may indirectly affect child health outcomes through changes in economic and nutritional conditions.

C. Government Health Spending

To assess whether fiscal pressures from serial restructurings influence government health spending, the analysis uses log-transformed government health spending as the dependent variable. The initial model examines the direct impact of restructurings while controlling for total debt service, GDP per capita, and inflation. A subsequent model adds FDI inflows to account for external financial contributions, which may affect government spending decisions. These models attempt to highlight the fiscal trade-offs that governments face during restructuring episodes.

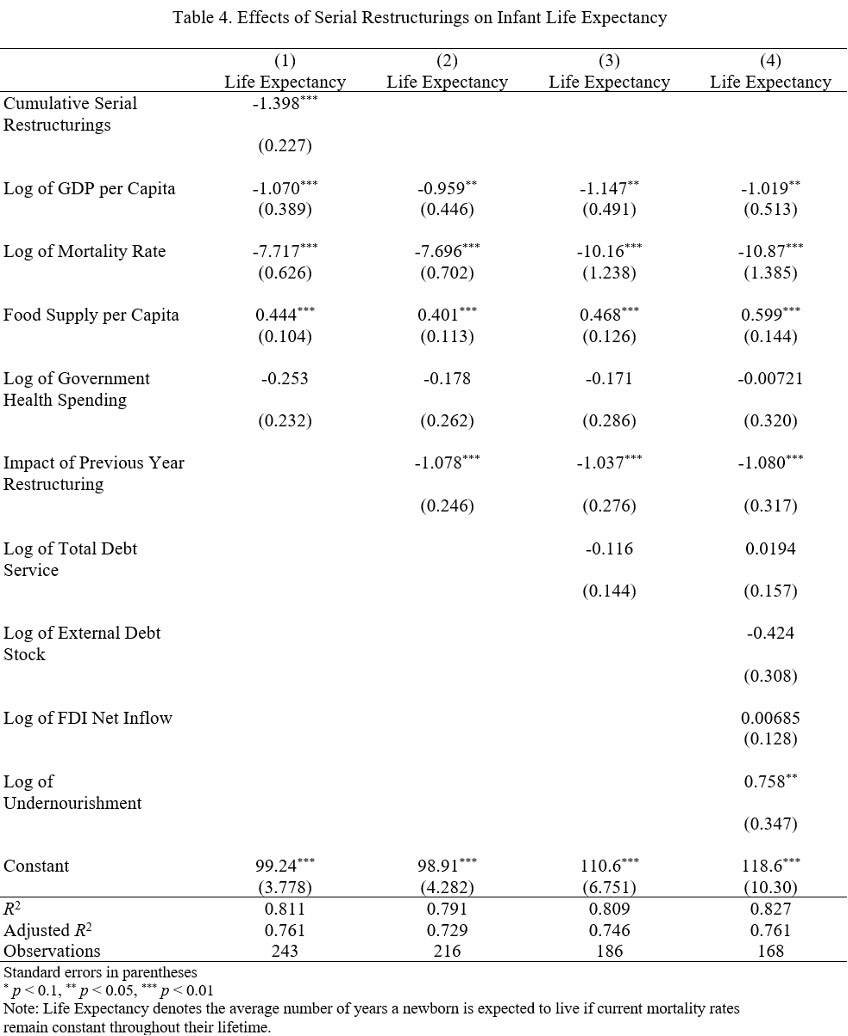

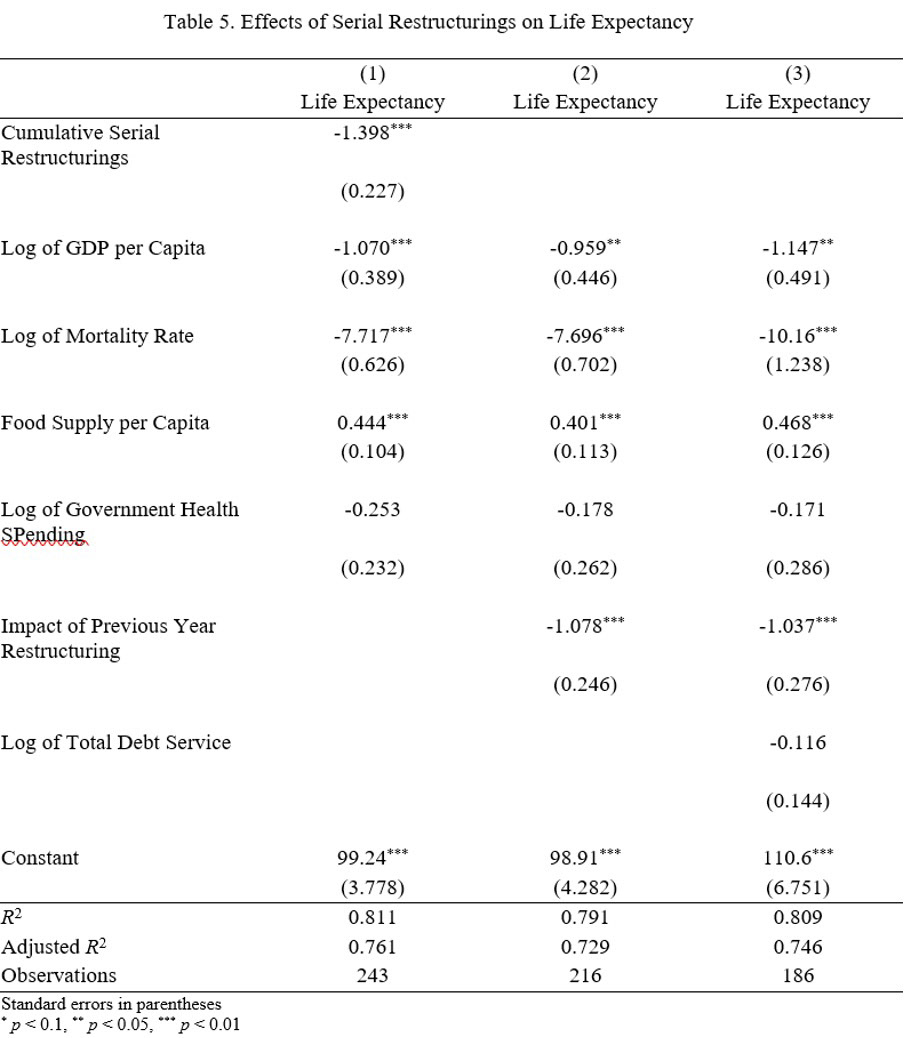

D. Infant Life Expectancy

Life expectancy is analyzed as a measure of long-term developmental outcomes influenced by serial restructurings. The initial model examines the contemporaneous effect of restructuring, while subsequent models introduce a lagged restructuring variable to account for delayed effects. Control variables include GDP per capita, mortality rates, food supply per capita, and government health spending. Additional models incorporate total debt service, external debt stock, foreign direct investment inflows, and undernourishment, capturing the macroeconomic and structural conditions that influence life expectancy. The final specification includes a comprehensive set of controls, allowing for a holistic examination of how fiscal and social factors mediate the effects of restructurings on life expectancy. Marginal effects and margins plots are used to visualize the temporal dynamics of restructuring impacts.

V. Data Analysis

A. Infant Mortality Rate

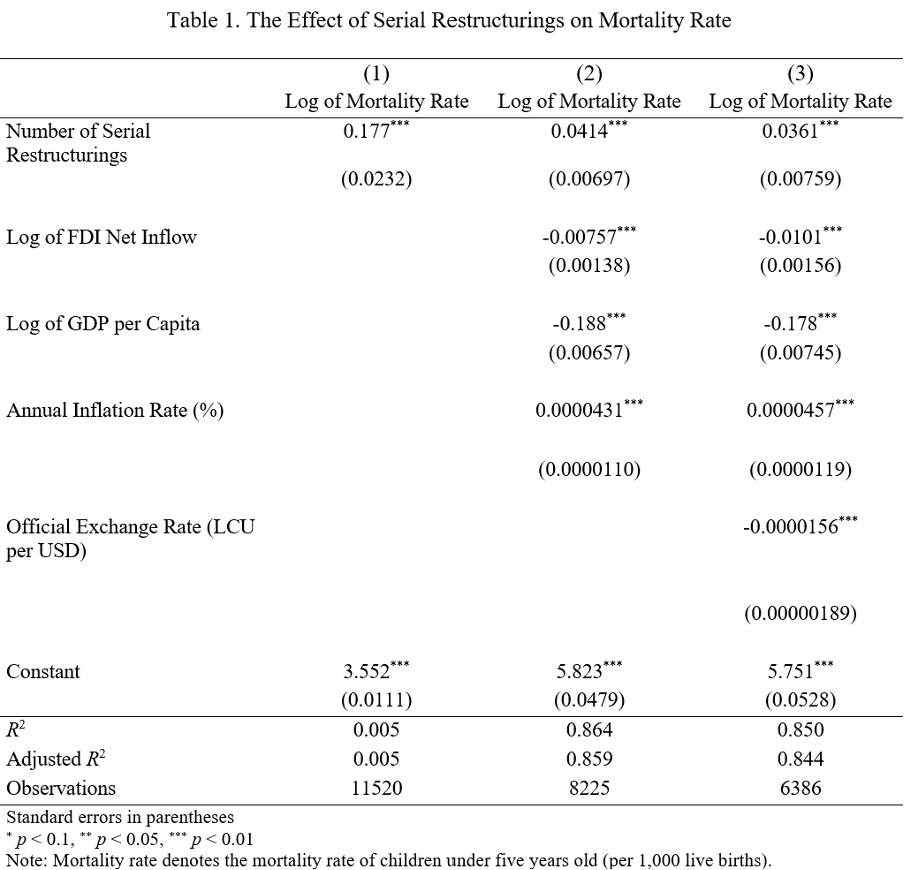

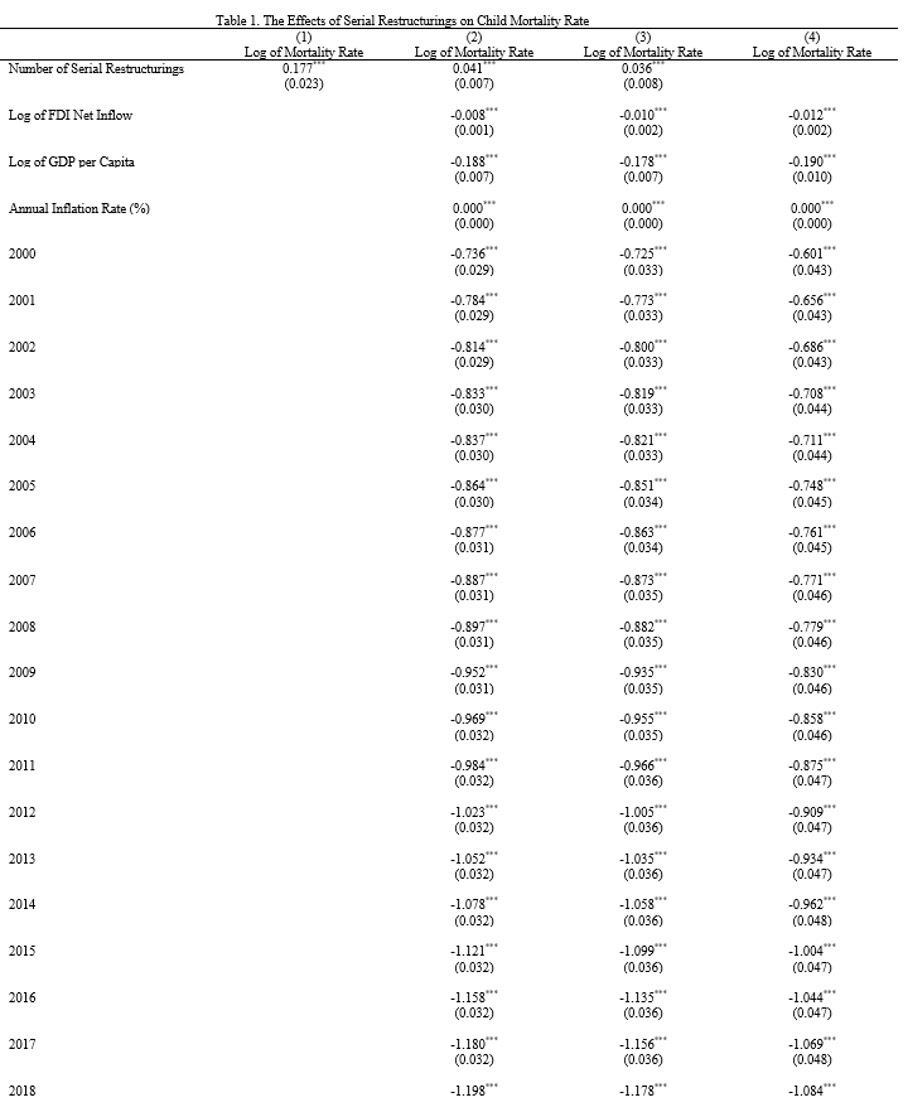

The regression results demonstrate a significant relationship between serial debt restructurings and child mortality rates, measured as the number of deaths of children under five years old per 1,000 live births. Since the dependent variable is log-transformed, the coefficients represent percentage changes, which can be translated into tangible impacts on mortality rates.

In Model 1, which uses an OLS regression, the coefficient for serial restructurings is 0.177, corresponding to a 19.4% increase in child mortality rates for each additional restructuring. For a country with a baseline child mortality rate of 50 deaths per 1,000 live births, this implies approximately 10 additional child deaths per 1,000 live births for each restructuring. While this model provides a basis for establishing a relationship between restructurings and child mortality, it does not account for unobserved country-specific factors or global shocks that could influence mortality rates. Subsequent models address these limitations by incorporating fixed effects and additional controls. In Model 2, after accounting for macroeconomic factors such as GDP per capita, foreign direct investment inflows, and inflation, the coefficient for serial restructurings decreases to 0.041, translating to a 4.2% increase in child mortality rates for each additional restructuring. In Model 3, which incorporates additional controls for exchange rates, the coefficient for serial restructurings further declines to 0.036, meaning that each additional restructuring is associated with a 3.7% increase in child mortality rates. This translates to approximately 2 additional child deaths per 1,000 live births. While the inclusion of these controls reduces the observed effect, the relationship remains significant, underscoring the persistent burden of serial restructurings on child health outcomes.

Model 4 adds an interaction term between serial restructurings and total debt service, providing deeper insights into how fiscal pressures influence the relationship between restructurings and child mortality rates. The base effect of each restructuring remains approximately 3.7%, or 2 additional deaths per 1,000 live births. However, the interaction term reveals that higher debt service obligations amplify the adverse effects as the number of restructurings increases. For instance, at three restructurings with high debt burdens, the combined impact leads to a 13.6% increase in child mortality rates, equivalent to roughly 7 more child deaths per 1,000 live births. This demonstrates how compounded effects of restructurings and fiscal constraints strain public health systems, worsening child health outcomes.

Control variables reinforce the importance of broader economic conditions. GDP per capita consistently shows a strong negative relationship with child mortality rates, with a 1% increase in GDP per capita associated with a 19% reduction in mortality rates. FDI inflows are similarly associated with lower mortality rates, indicating that external financial flows support improved health outcomes. Inflation, while small in magnitude, has a consistent positive association, reflecting the destabilizing effects of economic instability on child health.

Ultimately, serial restructurings are significantly associated with higher child mortality rates, with the adverse effects intensifying as the number of restructurings increases. The compounding impact of repeated restructurings, particularly in countries with high debt burdens, imposes serious challenges for child health and survival. For a typical country undergoing one restructuring, the result is approximately 2 additional deaths per 1,000 live births, but this rises to 7 additional deaths when compounded by repeated crises and fiscal constraints. These findings underscore the need for policies that minimize the social costs of restructurings and address the long-term developmental impacts on vulnerable populations.

B. Prevalence of Anemia

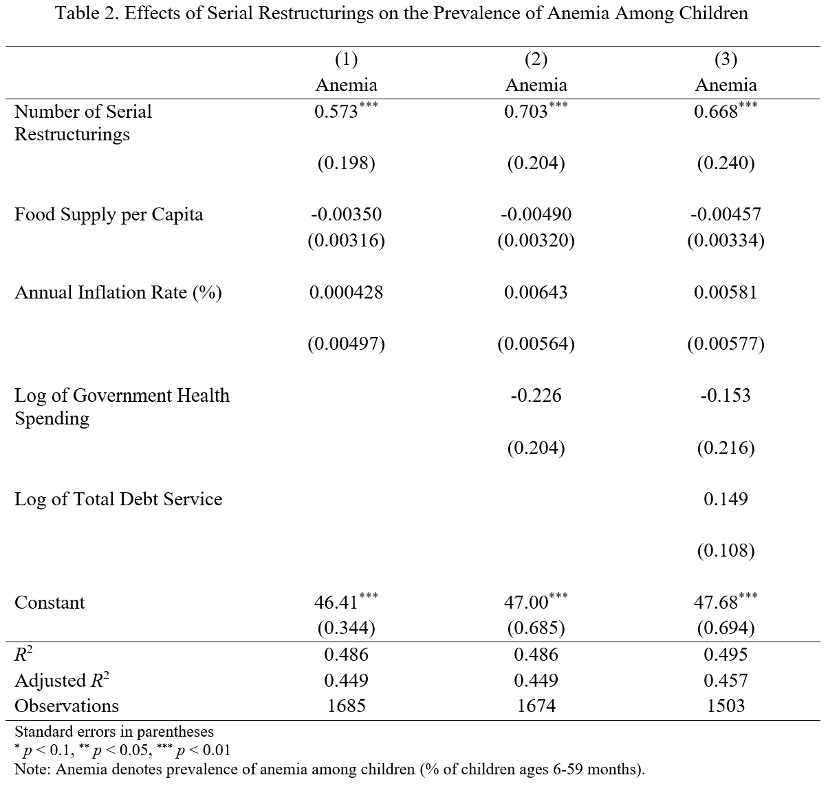

Serial restructurings exhibit a consistently strong positive relationship with anemia prevalence. In Model 1, the coefficient for serial restructurings is 0.573, indicating that each additional restructuring is associated with an increase of 57.3 percentage points in anemia prevalence. As additional controls are introduced in subsequent models, the effect size increases slightly. In Model 2, which includes government health spending, the coefficient rises to 0.703, translating to an increase of 70.3 percentage points in anemia prevalence for each additional restructuring. In Model 3, after adding total debt service as a control, the coefficient decreases to 0.668, showing a 66.8 percentage-point increase in anemia prevalence per restructuring.

The regression results suggest a strong relationship between serial restructurings and anemia prevalence among children under five years old, but the lack of significance for other control variables invites skepticism about the mechanism driving this relationship. Using a baseline anemia prevalence of 40%, which aligns with global averages in many low- and middle-income countries, and a population of 10 million children under five years old, this equates to 4 million children who are initially anemic. The compounding effects implied by multiple restructurings appear extreme and may reflect model overestimation. In Model 1, two restructurings result in a theoretical increase of 114.6 percentage points (from 40% to 154.6%), which exceeds plausible population limits. This suggests the model might be capturing exaggerated effects due to collinearity or insufficient adjustments for lagged impacts of prior restructurings. Another possible explanation is that serial restructurings act as a proxy for deeper systemic health vulnerabilities that are not captured by these variables. For example, countries undergoing multiple restructurings may already face persistent deficiencies in healthcare delivery, nutritional programs, and infrastructure that disproportionately affect children under five. These long-standing structural issues might not be reflected in year-to-year variations in spending or inflation, but restructurings exacerbate these pre-existing conditions, magnifying the observed effects on anemia.

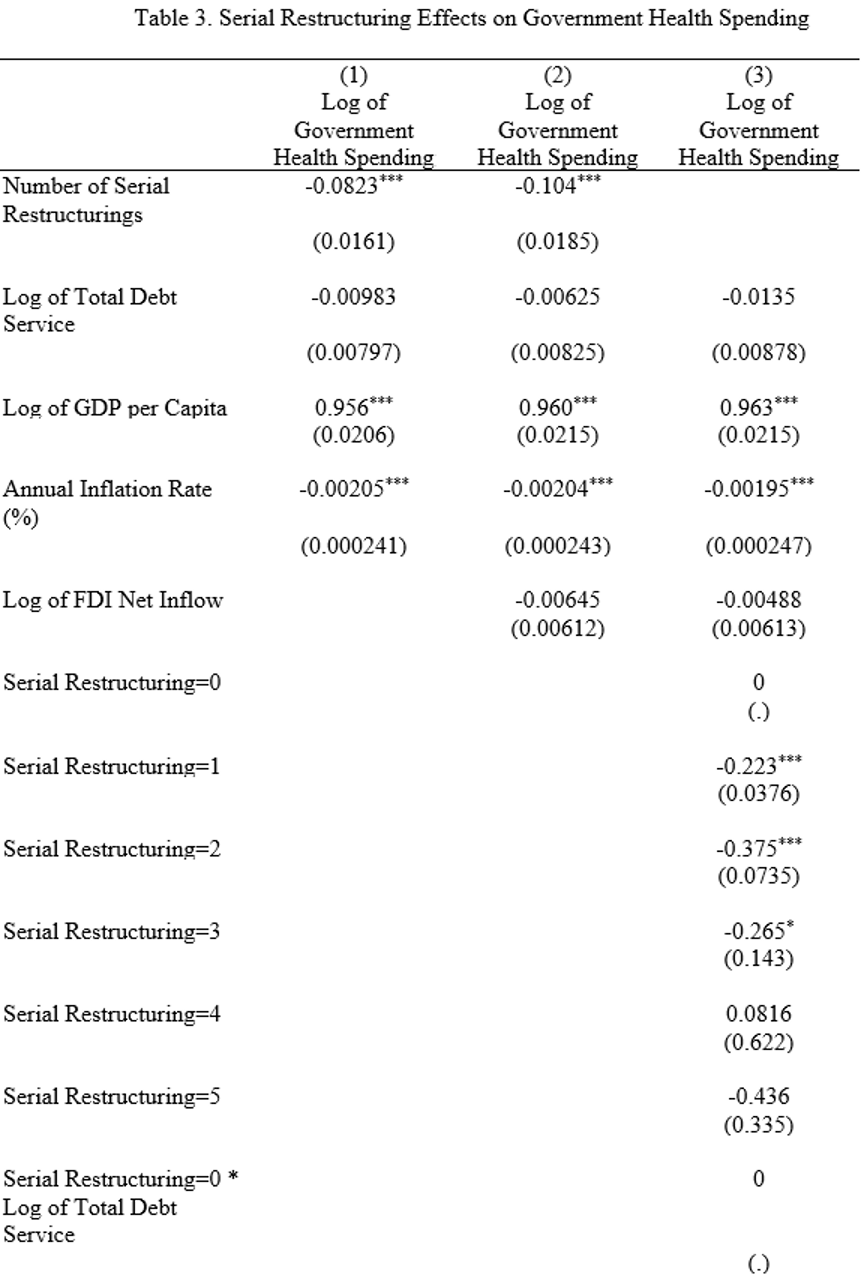

C. Government Health Spending

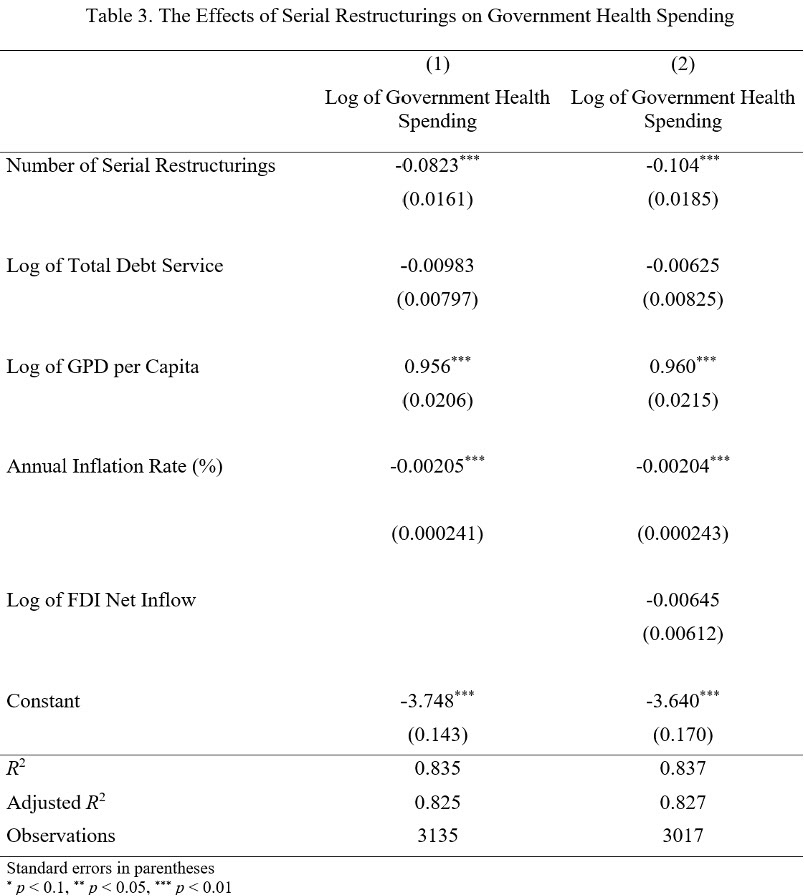

The regression results in Table 3 reveal the significant impact of serial restructurings on government health spending, measured as the log of public health expenditure. Serial restructurings show a strong and negative relationship with health spending, with coefficients of -0.082 in Model 1 and -0.104 in Model 2, both significant at the 1% level. This indicates that each additional restructuring is associated with an 8.2% to 10.4% reduction in government health spending. These reductions highlight how restructurings compound fiscal pressures, likely forcing governments to reallocate limited resources away from health services to address debt obligations or other fiscal priorities.

The results also underscore the critical role of economic conditions in shaping health spending. The log of GDP per capita has a strong positive association with health spending, with coefficients of 0.956 in Model 1 and 0.960 in Model 2. This implies that a 1% increase in GDP per capita is associated with a nearly 1% increase in health spending, emphasizing how economic development supports the ability of governments to invest in public health. By contrast, inflation has a small but statistically significant negative effect, suggesting that higher inflation erodes real spending power and creates additional fiscal instability.

The negative association between serial restructurings and health spending aligns with broader structural vulnerabilities discussed earlier. Countries undergoing repeated restructurings often face persistent fiscal constraints, even in the absence of broader economic crises or political instability. These constraints likely stem from weakened revenue collection, reduced access to external financing, and higher borrowing costs, all of which further limit governments’ ability to maintain essential public services. The findings suggest that restructurings exacerbate pre-existing structural deficiencies, forcing difficult trade-offs in public spending and disproportionately impacting critical sectors like health. The strong positive relationship between GDP per capita and health spending highlights the disadvantage faced by low-income countries, which often lack the economic resilience needed to sustain health investments during fiscal crises. The reductions in health spending revealed in this analysis are consistent with the earlier findings on child health outcomes, including anemia prevalence and child mortality. Declining health budgets undermine governments’ ability to deliver health services, exacerbating vulnerabilities in already fragile populations. Serial restructurings deepen these challenges, reinforcing a cycle of fiscal strain and declining public health investment. These results underscore the need for targeted policies to protect public health budgets during fiscal crises.

D. Infant Life Expectancy

The regression results in Table 4 provide valuable insights into how serial restructurings affect life expectancy, measured as the average number of years a newborn is expected to live if current mortality rates remain constant. Each coefficient represents the estimated effect of a one-unit change in the independent variable on life expectancy.

Model 1 shows that cumulative serial restructurings have a significant and negative impact on life expectancy. The coefficient for cumulative restructurings is −1.398, indicating that each additional restructuring reduces life expectancy by 1.4 years. For instance, in a country with an initial life expectancy of 70 years, one additional restructuring would reduce this figure to 68.6 years. This result underscores the immediate developmental costs of restructurings, likely reflecting disruptions to healthcare, nutrition programs, and public services. Among the control variables, the log of GDP per capita is associated with a −1.070 decrease in life expectancy for every 1% increase in GDP per capita. This unexpected negative relationship may reflect economic volatility during restructuring periods, where increased GDP per capita does not translate into equitable or health-promoting resource distribution. The log of mortality rate has a significant negative coefficient of −7.717, meaning a 1% increase in the mortality rate reduces life expectancy by approximately 7.7 years, which is expected given the direct relationship between mortality and longevity. Food supply per capita has a positive coefficient of 0.444, suggesting that an additional unit of food supply increases life expectancy by 0.44 years, emphasizing the importance of nutrition in improving health outcomes. However, government health spending is not significant, implying that spending alone does not directly improve life expectancy within the context of restructurings.

Model 2 incorporates a lagged restructuring variable to capture the delayed effects of restructurings on life expectancy. The coefficient for the lagged restructuring variable is −1.078, indicating that a restructuring in the previous year reduces life expectancy by 1.08 years. For example, if a country's life expectancy was initially 70 years, a restructuring event would lower it to 68.92 years in the following year. This reflects the persistent negative effects of restructurings, which may result from prolonged fiscal austerity, reduced public services, or weakened health systems. The coefficient for the log of GDP per capita is −0.959, suggesting that a 1% increase in GDP per capita is associated with a 0.96-year reduction in life expectancy. This counterintuitive result might indicate that during restructuring periods, increases in GDP per capita do not necessarily translate into broad societal benefits, potentially reflecting rising inequality or misallocation of resources. The log of mortality rate has a significant negative coefficient of −7.696, meaning that a 1% increase in mortality rate corresponds to a 7.7-year decrease in life expectancy, highlighting the direct relationship between higher mortality and shorter life spans. Food supply per capita has a positive coefficient of 0.401, indicating that a one-unit increase in food supply raises life expectancy by 0.40 years, or roughly 4.8 months, reinforcing the importance of adequate nutrition. Government health spending remains insignificant, suggesting that the quantity of spending alone may not drive health outcomes, potentially due to inefficiencies or insufficient targeting.

Model 3 introduces total debt service as an additional control to account for fiscal burdens associated with debt repayment. The coefficient for total debt service is −0.116, but it is not statistically significant, suggesting that variations in debt repayment obligations do not directly explain life expectancy changes when other factors are included. The lagged restructuring variable remains significant, with a coefficient of −1.037, meaning that each restructuring in the previous year reduces life expectancy by 1.04 years. For example, in a country with an initial life expectancy of 65 years, this would decrease life expectancy to 63.96 years following a restructuring. Food supply per capita continues to have a positive association with life expectancy, with its coefficient increasing to 0.468. This means that a one-unit increase in food supply raises life expectancy by approximately 0.47 years, or just over 5.6 months, underscoring the critical role of nutrition in improving health outcomes, especially during periods of economic stress. The log of GDP per capita remains negative and significant (−1.147), meaning that a 1% increase in GDP per capita reduces life expectancy by 1.15 years, reinforcing the earlier suggestion that economic growth during restructuring periods may not translate into improved societal well-being. The mortality rate continues to have a strongly negative impact, with a coefficient of −10.16, indicating that a 1% increase in mortality rate reduces life expectancy by over 10 years, reflecting its dominant influence on population health.

Model 4 incorporates additional controls, including external debt stock, FDI inflows, and undernourishment, to provide a more comprehensive view. The lagged restructuring variable remains significant (−1.080), meaning that a restructuring in the previous year reduces life expectancy by 1.08 years, similar to the results in earlier models. This underscores the lasting developmental costs of repeated restructurings. The coefficient for external debt stock is −0.424, but it is not significant, suggesting that the overall level of external debt does not independently influence life expectancy within the model. The log of FDI net inflows has a coefficient of 0.007, which is also insignificant, indicating that foreign direct investment does not have a measurable impact on life expectancy in this context. The coefficient for undernourishment is 0.758, which is both significant and positive. This unexpected result may reflect improvements in targeted nutritional interventions during periods of restructuring, as governments or international agencies often prioritize addressing severe nutritional deficits in crisis-affected populations.

Across all models, the coefficients for restructurings consistently show significant negative effects on life expectancy, with lagged effects underscoring the persistence of these impacts. The results for GDP per capita and mortality rates highlight broader economic and demographic drivers, while the positive influence of food supply underscores the importance of addressing nutritional needs during fiscal crises. These findings emphasize the need for policies that protect public health and nutrition systems to mitigate the long-term developmental consequences of repeated restructurings.

VI. Robustness Tests

A. Infant Life Expectancy

To test the robustness of our findings, I compared fixed-effects and random-effects models to analyze the impact of serial restructurings on life expectancy. Fixed-effects models control for unobserved, time-invariant country-specific factors, such as geographic or institutional characteristics, and focus exclusively on within-country variation over time. In contrast, random-effects models incorporate both within-country and between-country variation, assuming that unobserved country-specific factors are uncorrelated with the independent variables. This assumption makes random-effects models more efficient but biased if the assumption is violated.

Both models yield consistent results regarding the core relationship: serial restructurings significantly and negatively impact life expectancy. In the random-effects model, the coefficient for cumulative restructurings in Model 1 is −1.398, indicating that each restructuring reduces life expectancy by 1.4 years—a result closely aligned with the fixed-effects estimate. Similarly, the lagged restructuring variable in Models 2 and 3 shows a significant reduction of about 1.08 years in life expectancy for each restructuring in the previous year, again mirroring the fixed-effects results. Control variables such as GDP per capita and mortality rates also demonstrate consistent effects. For instance, GDP per capita shows a counterintuitive negative relationship with life expectancy, with a 1% increase associated with a decrease of approximately 1 year. This result likely reflects structural challenges during restructuring periods, such as rising inequality or ineffective resource allocation. Mortality rates maintain a strong and expected negative association, with a 1% increase in the mortality rate reducing life expectancy by 7.7 to 10 years across models. Food supply per capita consistently exhibits a positive and significant relationship, with each unit increase contributing approximately 0.4 to 0.6 years to life expectancy, emphasizing its critical role in mitigating the adverse effects of restructurings.

While the overall results are consistent, there are notable differences between the models. Random-effects models allow for between-country variation, leading to slightly larger coefficients for some control variables, such as mortality rates and food supply. Additionally, undernourishment emerges as significant in the random-effects model but not in the fixed-effects model, possibly due to differences in how cross-country variation is handled. Importantly, both models indicate that variables such as total debt service, external debt stock, and FDI inflows do not significantly affect life expectancy, suggesting these factors play a limited direct role in shaping health outcomes during restructuring periods.

To ensure the appropriateness of the random-effects model, a Hausman test will be conducted at a later stage to compare the two approaches. If the test favors fixed effects, it will confirm that fixed effects are more robust to omitted variable bias, making them the preferred method. Alternatively, if the test supports random effects, it will validate their efficiency in leveraging between-country variation. Regardless, the consistency of key findings across both models supports the robustness of the results.

VII. Conclusion

This paper provides new insights into the long-term social and fiscal consequences of serial restructurings, focusing specifically on China's debt restructuring practices from 2000 to 2020. By examining the relationships between serial restructurings and key health and welfare indicators—child mortality rates, anemia prevalence, government health spending, and life expectancy—this study bridges critical gaps in the existing literature, which has historically centered on economic outcomes like GDP growth while neglecting broader social costs.

The key findings underscore the substantial and persistent developmental costs associated with serial restructurings. Each restructuring is associated with a 3.7% increase in child mortality rates, translating to approximately 2 additional child deaths per 1,000 live births for a country with a baseline rate of 50 deaths. Life expectancy declines by 1.4 years per restructuring, with lingering effects reducing it by an additional 1.08 years in the subsequent year. Anemia prevalence rises sharply—by 57.3 to 70.3 percentage points per restructuring—though this extreme result likely reflects the cumulative vulnerability of countries with fragile healthcare systems. On fiscal outcomes, government health spending declines by 8.2% to 10.4% per restructuring, highlighting the significant trade-offs governments face between servicing debt and maintaining critical public health investments. Collectively, these findings illustrate the broad and enduring social costs of restructurings, which compound over time, amplifying adverse outcomes for vulnerable populations.

The implications of these findings are profound. Serial restructurings exacerbate the challenges faced by debtor nations, perpetuating cycles of fiscal strain and undermining public health systems. These effects are especially troubling for low-income countries that lack the institutional capacity to cushion their populations against the compounded impacts of fiscal austerity and systemic underinvestment in health and nutrition. The results also call into question the long-term efficacy of "no-haircut" restructuring strategies that prioritize short-term liquidity relief over meaningful debt resolution. By prolonging debt cycles and intensifying fiscal pressures, these strategies impose significant social costs that threaten the developmental trajectories of debtor nations.

Despite these contributions, this paper leaves important questions unanswered, creating opportunities for further research. First, the mechanisms underlying the observed effects on anemia prevalence and life expectancy remain unclear. Future work could explore whether these outcomes stem directly from fiscal constraints or whether they reflect deeper structural vulnerabilities in healthcare delivery and public services. Additionally, while this study focuses on serial restructurings, it does not account for potential differences in outcomes between first-time and repeat restructurings. Understanding whether the developmental costs of initial restructurings differ from those of subsequent ones could offer valuable insights for policymakers. Lastly, this paper focuses on the debtor-side effects of serial restructurings. Examining the creditor-side dynamics, such as the financial and geopolitical motivations behind restructuring strategies, would provide a more holistic understanding of the trade-offs involved. Ultimately, this study demonstrates that the social costs of serial restructurings are significant, broad-based, and enduring. It underscores the need for policies that prioritize sustainable debt solutions while safeguarding public health and welfare in debtor countries. As China's role as a global creditor becomes more transparent, the long-term impacts of its lending and restructuring practices will remain a critical area for future inquiry.

Appendix

Figure 2. Comparison of Scope of Debt Relief: China, Paris Club, and Private Creditors

Figure 3. Restructurings with Low-Income Countries (1970 - 2022)

Figure 4. Restructurings with Emerging Economies (1970 - 2022)

Figure 5. China's Total Net Debt Transfers (2000 - 2020)

References

reference 1: See Figure 2. Comparison of Scope of Debt Relief: China, Paris Club, and Private Creditors in Appendix.

reference 2: See Figure 3 and Figure 4 in Appendix.

reference 3: Clemens M. Graf von Luckner, Josefin Meyer, Carmen M. Reinhart, and Christoph Trebesch, Sovereign Haircuts: 200 Years of Creditor Losses, NBER Working Paper No. 32599 (Cambridge, MA: National Bureau of Economic Research, June 2024), https://doi.org/10.3386/w32599.

Bibliography

Asonuma, Tamon, Marcos Chamon, and Aitor Erce. 2019. "Sovereign Debt Restructurings and Economic Outcomes: A Quantitative Assessment." Journal of International Economics 119 (May): 179–98. https://doi.org/10.1016/j.jinteco.2019.01.007.

Easterly, William, and Stanley Fischer. 2004. "Inflation and the Poor." Journal of Money, Credit, and Banking 34 (1): 160–78. https://doi.org/10.1353/mcb.2004.0007.

Graf von Luckner, Clemens M., Josefin Meyer, Carmen M. Reinhart, and Christoph Trebesch. Sovereign Haircuts: 200 Years of Creditor Losses. NBER Working Paper No. 32599. Cambridge, MA: National Bureau of Economic Research, June 2024. https://doi.org/10.3386/w32599.

Horn, Sebastian, Carmen M. Reinhart, and Christoph Trebesch. 2020. "China’s Overseas Lending." Journal of International Economics 133 (November): 103496. https://doi.org/10.1016/j.jinteco.2020.103496.

Reinhart, Carmen M., and Kenneth S. Rogoff. 2009. This Time Is Different: Eight Centuries of Financial Folly. Princeton, NJ: Princeton University Press.

Das, Udaibir S., Michael G. Papaioannou, and Christoph Trebesch. 2012. "Sovereign Debt Restructurings 1950–2010: Literature Survey, Data, and Stylized Facts." IMF Working Paper No. 12/203, International Monetary Fund. https://doi.org/10.5089/9781475505516.001.